Asset productivity drives the engine of efficient companies over the long term, writes Ted Black

THE share market and the pressures it creates for top management is a significant, topical issue raised in the latest McKinsey Quarterly Review (Richard Rumelt, Strategy’s Strategist). Generous share-option schemes can aggravate the problem, stimulating managers to pursue the wrong goal.

As we know, prices are volatile. They respond to speculative expectations about future changes in industry and market sectors — less so to individual company performance. Top managers may think that’s unfair, but what does it mean for them?

They have to grit their teeth and detach themselves. They must play the ball, not the market players. They must stop pandering to analysts; ignore short-term share-pricemoves and perform their prime threefold management task, which is to: n Make today’s business viable; n Identify and release its hidden reserve of potential; and n Turn it into tomorrow’s business. Do these three things well, and the numbers will follow—not least the share price. We know that the valuation mechanisms of professional investors and analysts can be hugely inefficient for a long time. However, in the end, performance power counts. It is the most important power of all. For a company, a key driver of it is asset productivity. High productivity buys you the time and leisure to think creatively —a rare activity for most people in most organisations. Thinking people make assets work. When they work, they generate cash. Cash creates options and opportunities. Seize them and you leave competitors trailing as you take charge of your own destiny —your growth and evolution. The first trait of the long-lived companies that Arie de Geus described 10 years ago in his book, The Living Company, was conservative financing. Extraordinarily successful companies do not risk money needlessly. They understand the meaning and value of cash in the bank.

The three most important financial measures of operating management are:

- Return on assets managed (ROAM) — the total profit of the business. This is

- Profit margin (operating profit divided by sales multiplied by 100), multiplied by

- Asset productivity, or asset turnover (sales divided by assets).

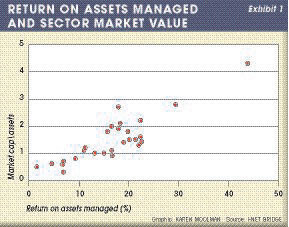

Using the latest year-end numbers, Exhibit 1 is a snapshot using data from more than 100 companies in 27 sectors on the Johannesburg Stock Exchange. It compares ROAM performance to a measure of value creation.

It shows clearly a strong, positive correlation between ROAM performance and the ratio of market capitalisation to assets managed. As ROAM rises, so does the perceived value of the sector.

However, as Boston Consulting Group pointed out as recently as 2003 in its Value Creators Report, Back to Fundamentals, the measure in ROAM that is most significant from a competitive viewpoint is asset productivity (asset turnover, or ATO in accounting jargon). It drives ROAM and, fundamentally, the value of a firm.

Its findings showed that the days of relying on “expectation premiums” to fuel total shareholder returns are over. They argue that these premiums eventually decline to their long-term market average of zero. Only firms with strong fundamentals can achieve superior returns. Moreover, the top performers rely on asset productivity more heavily than cash-flow margins to lift profitability.

To back that view, a momentous but predictable event occurred this year. Toyota passed General Motors (GM) to become the biggest, most profitable car manufacturer in the world. However, a warning light flashed on more than 25 years ago.

Toyota landed a car from Japan outside GM’s HQ in Detroit at better quality and a lower delivered cost than GM could achieve in the US.

Ironically, that’s when Tom Peters launched his career as a management guru and hyped GM as an excellent company in his, and Robert Waterman’s, blockbusting In Search of Excellence.

Exhibit 2 shows a major reason why Toyota is the leader today.

The latest results (car-making only) illustrate the relative, competitive ATO effect. Toyota’s asset productivity, with Tata close on its heels, is about 60% higher than the rest. It has been way ahead of GM for years.

Firms worldwide are now applying its manufacturing principles, not only in production plants, but also in service industries wherever managers are determined to drive waste out of business systems and change the way their people work together.

We applaud management heroes who rescue companies. However, few of them build sustainable businesses. They bring some order, then move on. In contrast, the truly successful companies have no heroes.

Very few of us can name the man who runs Toyota. As Jim Womack, coauthor of Lean Thinking puts it, its success comes through the work of lots of “farmers”, not heroes. These farmers are people who plough straight furrows, fix fences and keep a beady eye on the weather.

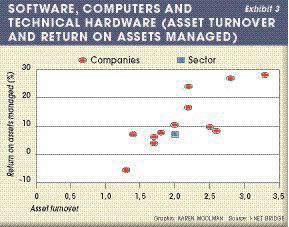

Moving back to SA, there were many heroes in the information technology sector a few years ago. Most IT companies are not highly valued today.

Overall, the sector’s market capitalisation to assets managed ratio is 0.7, despite a booming market. Exhibit 3 displays its performance.

Again, the ATO effect is clear. Datatec, Didata and Business Connexion account for 85% of the assets managed. Their combined ROAM is 6% — a very mediocre result. The top performer is Paracon, but its core business is to find and place IT people — not sell software, implement systems or “drop boxes”.

As to Didata, the boys from Roosevelt High have learned the truth of Virgil’s maxim from the Aeneid (Book 6): “Facilis discensus averim… Sed revocare gradum …Hoc opus, hic labor est” — the descent (to hell) is easy …but to recover one’s steps … that’s the task and effort.

Once you’re on the slippery slope, it’s all hell to get back again.

It is easy to be carried away with hubris, but ego can stop top management from doing much needed weeding and pruning in the garden even though the numbers tell them to do it. Half of Didata’s asset base generates 37% of sales, but 74% of the operating profit. The rest of the assets generate 63% of sales and only 26% of the profit. To make matters worse, the poor performers probably attract more than 80% of the central costs of $34,5m that wipe out their contribution anyway.

And the final message from this sector? A recent Financial Mail article about Business Connexion says it all: “The move to a business management software system from SAP had a material adverse impact on the collection of trade debtors.” So much for asset productivity.

One can only wonder about the number of companies that have been whacked by SAP-wielding IT people who do not seem to understand what productivity is or know how to use their technology to make a measurable impact on it. Their systems seem to tighten, instead of prising off the throttling grip of bureaucracy ’s dead hand.

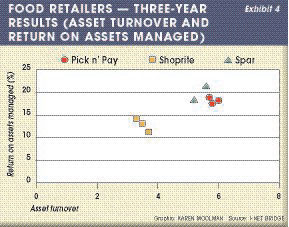

Then we move into the retailers. Exhibit 4 compares the relative asset productivity and ROAM of the big three food retailers in SA. Until its latest results, Shoprite trailed Spar and Pick ’n Pay with both measures. Its sales margin has lifted ROAM, but not enough to catch up.

There is a lot we can learn about business design and supply-chain management from these big retailers —some of it not always good. There are suppliers who would prefer to deal with terrorists — at least you can negotiate with them, they say.

However, in contrast to the traditional, confrontational buying approach of most firms, Wal-Mart in the US raced ahead of Kmart during the early 1990s by paying its suppliers sooner and working closely with them. Faster inventory turn led to better instore product availability. This meant they sold more, which pushed up sales per square metre and fixed asset productivity.

To achieve these improvements, management chose a measure that Wal-Mart’s then 1-million employees would understand. That criterion eliminated EVA™(economic value added) and CFROI (cash flow return on investment) as measures. They wanted something that everybody could grasp easily and commit to —it was ROAM.

The effect was dramatic. Over a three-year period, sales increased 47%, but inventories grew only 7%.

Taiichi Ohno, Toyota’s legendary plant manager, was the architect of the company’s manufacturing system. He visited Ford Motor Company before and after the Second World War. He found no change the second time and learned nothing from his trip.

However, while there, he walked into a supermarket for the first time. The experience sparked Toyota’s asset productivity-driven design. He switched it from “push” to “pull” production, and knew that suppliers had to become a key part of that shift in strategy. Today, Toyota’s business model is the machine that is changing the world.

If retail and IT companies are asset-light, what about capitalintensive industries such as mining? The sector’s market cap/assets ratio is 2.1 and individual companies are plotted in Exhibit 5.

The picture is the same. ATO drives up ROAM. Kumba and Lonmin lead the pack. Harmony and Anglo Gold bring up the rear.

The writing was on the wall for Harmony in 2004. Management’s strategy doubled up the asset base and halved its productivity. It has bumped along or below the line at the bottom left-hand corner of the chart ever since.

As to one of SA’s exemplar companies, Exhibit 6 compares SABMiller ’s various business units with each other and for further comparison, includes Anheuser Busch’s and Molson Coors’ North American beer interests.

Yet again, the asset productivity effect is clear. We can only hope that management doesn’t fall prey to ego, and match weakness with opportunity as it did when buying Miller, and compound the problem by merging it with Molson Coors. Adding low-performing assets to low-performing assets — doubtless at a hefty premium —will plunge it deeper in the North American swamp and guarantee failure.

As to taking SABMiller on in SA with Amstel, Heineken could be careering into a swamp here. On the chart, the South African business unit includes ABI. If we could take it out and look at asset productivity of beer alone, it’s a safe bet that ATO and ROAM will be right off the chart.

SAB can crush anyone who tries to enter this market. However, instead of going to Sun City for a gig costing millions of rands to work its sales and marketing people up into a competitive frenzy, it might be in the company’s interests (and shareholders’ for that matter) to adopt a more “statesmanlike” approach.

An “orderly ” beer war might not be such a bad thing. They don’t have to maul each other like Miller and Bud are doing. Instead, a well orchestrated arrangement (kept top secret, of course) could see all beer sales going up as consumers join in the fray “chug-a-lugging” their favourite brands. It won’t happen though. As Joseph Bower wrote 20 years ago in When Markets Quake: “The willingness of companies to bleed each other is awesome!”

If they do go to war, the company with the highest asset productivity will win. It can bleed for longer. Beer South Africa can bleed for a very long time if it has to.

Competitive ATO is why Miller is doomed to mediocrity in the US and why Heineken is taking such a big risk here — unless it has a sinister bloodletting plot with wider implications that we don’t know about.

So what does all this mean for management? The second characteristic of the long-lived companies that Arie de Geus identified was that no matter how diversified they were, their people felt they belonged.

Case histories showed that a “sense of community” is essential for long-term survival. The managers of living companies commit to people before assets because they know that people — not spreadsheets and pieces of paper—make assets work. Moreover, line managers must initiate the change process, not earnest corporate staff who behave as if they own the assets. They don’t. Line managers do.

Effective managers who believe in growing people and building a community know that you don’t do it in a classroom. You build communities of growing people most rapidly and sustainably when its members are “forced ”, so to speak, to develop it under short-term, concrete, real-life challenges that are important to them.

These challenges always lie at points of overlap along the value stream of activities from supplier through to customers. That’s where you find the largest performance improvement potential to lever up asset productivity and where you can design community building projects that grow members fast, furiously and measurably. The improvement in the number tells you how much they have developed and provides the building blocks for expansion of the process.

The long-lived companies commit to people first and assets second. People are “the horse” and asset productivity is “the cart”. All it needs is to educate your people in what it is. As we all know, very few of them do, and that’s true from boardroom to the work place.

It’s a wonderful message of opportunity.

Ted Black (jeblack@icon.co.za) writes, coaches and conducts ROAM workshops that help managers design results-driven projects that grow them and their people